It is estimated that 200 top mobile game distributors worldwide are losing approximately $41 million a day as they continue to direct most of the players ‘ consumption to an app store payment system of 30 per cent, instead of using a direct-company payment infrastructure at a rate close to 5 per cent. According to the report of the Global Payment and Business Platform Appcharge, based on millions of settlement sessions in the United States, Europe and Asia (over $700 million in trades), regulatory changes, the application of transfer payments and the increasingly sophisticated web-shop design are fundamentally reshaping the way players consume and the value acquisition model of distributors.

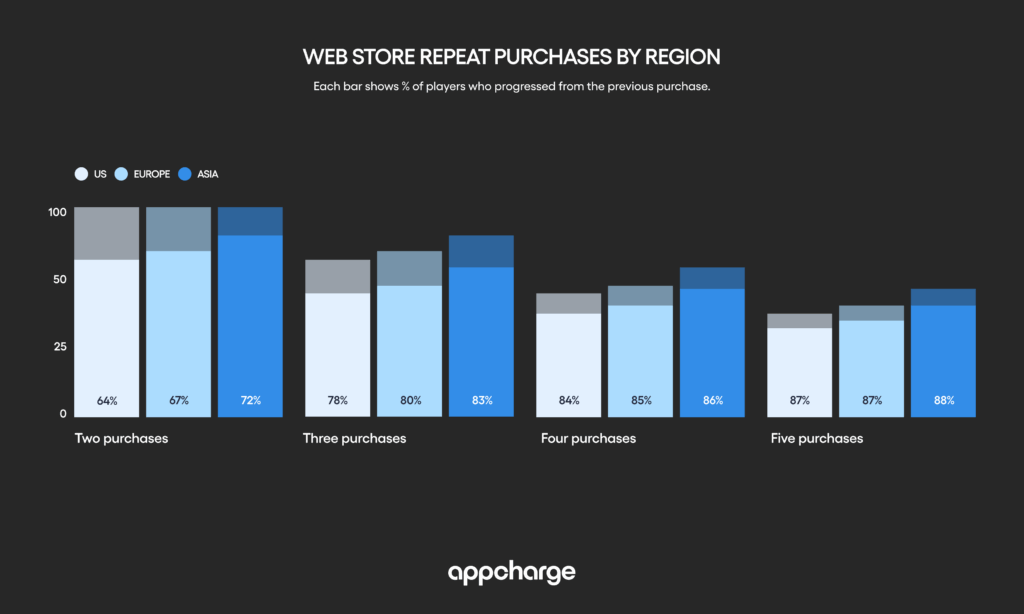

One of the most visible changes was that the application of the Internet-based payment link had become the most effective entry point for direct-link payments. The Appcharge data show that 56 per cent of the playhouses using payment links are new customers paid directly, and one quarter of them will be converted into web shop customers. The key is that the introduction of payment links does not erode the income of existing web shops, but can lead to incremental growth. The report states that, although the payment link opens the door for the player to pay directly, the web store is where the issuer achieves maximum long-term value. In Appcharge-supported shops, 97 per cent of the income comes from duplicate purchasers, with the average value of the order being three times as high as the value of the application. Once the player has completed three purchases in a web store, the global double-purchase rate exceeds 84 per cent, marking a shift in consumption behaviour from an occasional to a customary one.

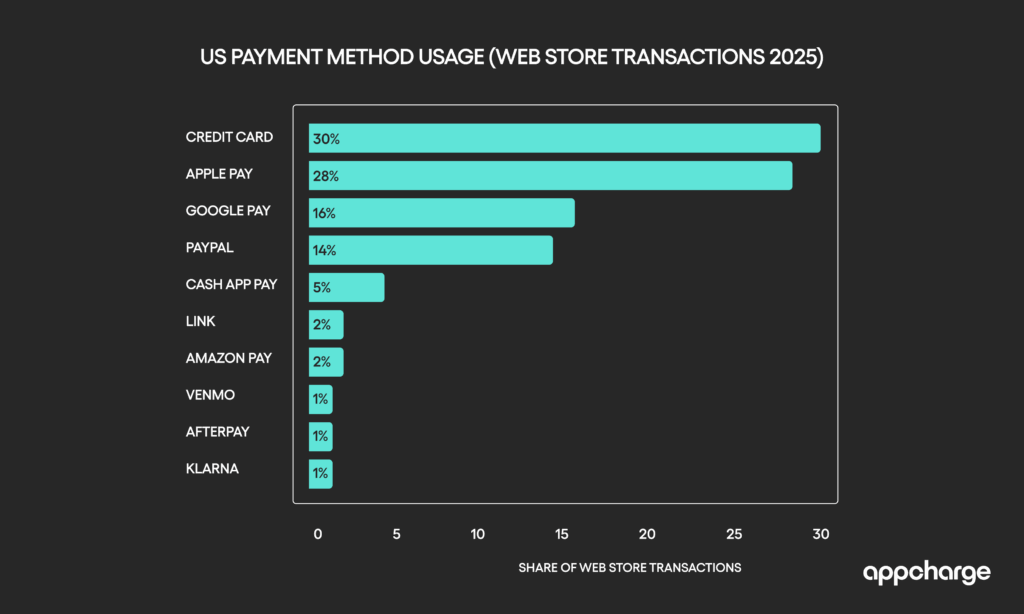

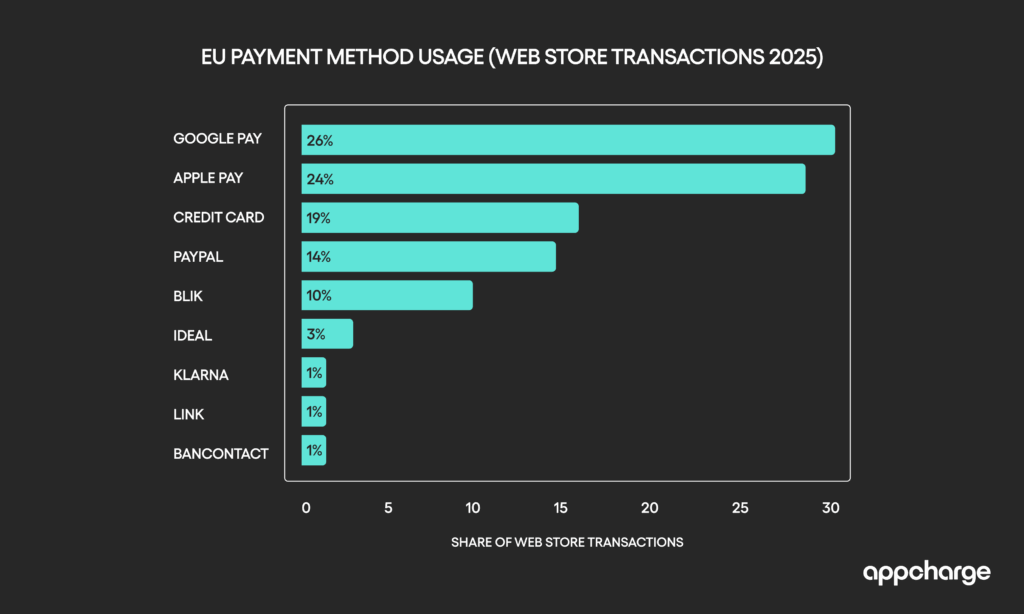

The data also show that straight-to-face consumption behaviour in hand-to-hand travel has now converged into real-time operating patterns, as opposed to non-traditional electric operators. Efficient web stores are designed and operated as real-time products, using mechanisms such as progress bars, rolling preferences and daily incentives to influence repetitive consumption behaviour and significantly increase the average income of paid users. Seasonal activities, in particular, have become powerful revenue growth points, such as black Fridays and Internet Mondays, which in a single day could result in a 50-60 per cent increase in income in web shops. In the United States, three modes of payment contributed about three quarters of the web store revenue, enabling the team to optimize around a small core. By contrast, Europe does not have any single payment modality in excess of 30 per cent, and local payment options have become key transformational points in specific markets.

Chief Executive Officer Maor Samon of Appcharge said: “Our data show that 2025 was a turning point, with the application of switch-to-page payments, the Web store, the alternative distribution channel, having evolved from a marginal case to an expansive and replicable revenue engine. The payment link opened the door, while the web store built the home. Successful distributors in the field of direct-company payments are viewing the web store as a real-time operational product — continuous optimization, personalization and deep association with player behaviour.” Looking ahead to 2026, the report concludes that, while the application of page-to-page payments will continue to play a supporting role, the next phase of the direct-to-company payment growth will be driven by web shops operating as long-term products and supported by their own distribution channels, such as e-mail, community platforms and the VIP programme.